How Annuities Work

Annuities involve a two-phase process:

- Accumulation Phase: You make payments to the insurer, and the money grows tax-deferred.

- Annuitization/Payout Phase: The insurer makes regular payments to you, either immediately (within a year) or at a future date.

Types of Annuities

- Fixed Annuity: Guaranteed, fixed interest rate and payments.

- Indexed Annuity: Interest is credited based on a market index (like S&P 500) with a minimum guarantee, often zero.

- Immediate vs. Deferred: Immediate annuities begin payments shortly after purchase; Deferred start later.

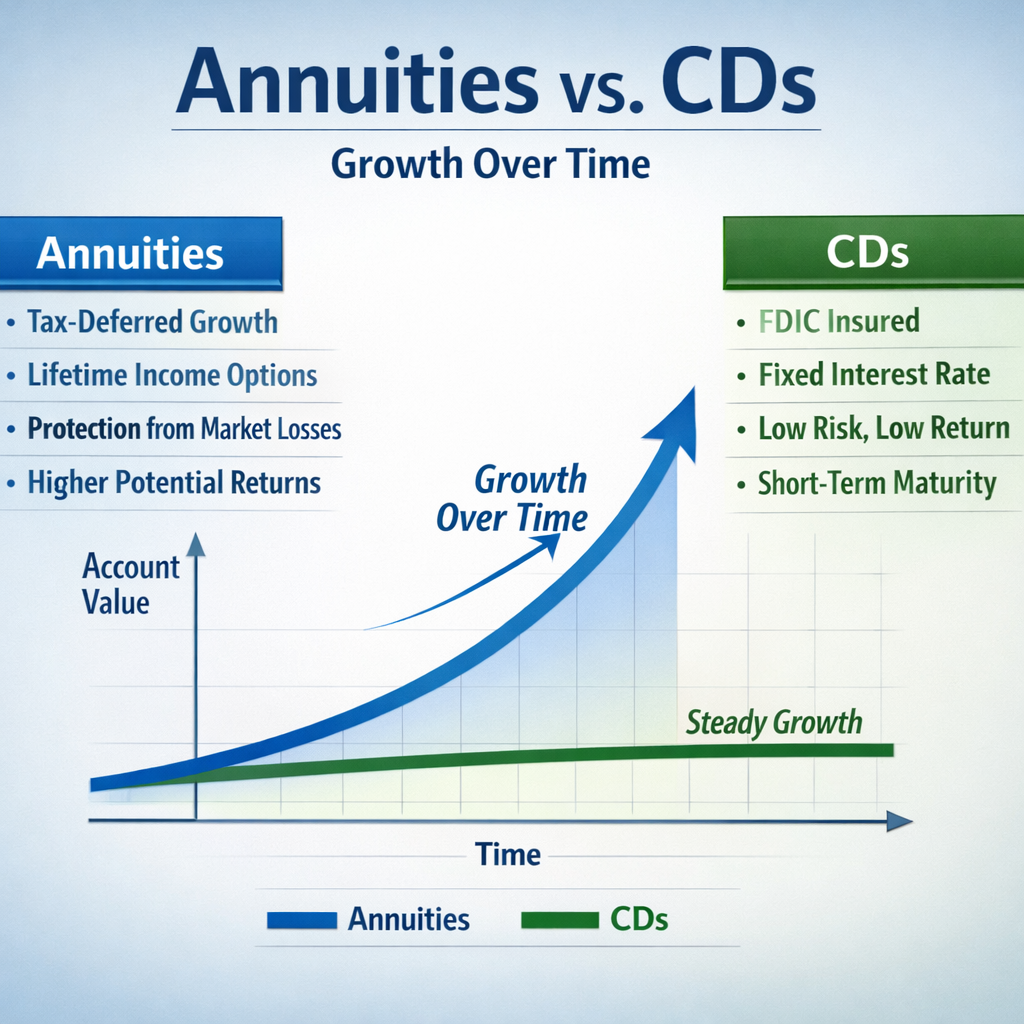

A MYGA (Multi-Year Guaranteed Annuity) is a type of fixed-rate annuity that allows you to lock in a guaranteed interest rate for a set number of years, typically 3 to 10 years. They are designed for conservative, tax-advantaged growth and are frequently described as the insurance industry’s version of a Certificate of Deposit (CD).

Advantages

- Lifetime Income: Protects against outliving savings.

- Tax-Deferred Growth: No taxes on earnings until withdrawal.

- Customization: Options for death benefits for beneficiaries.

- Safety: Fixed annuities protect against market losses.

When to Consider an Annuity

- You are close to or in retirement and need guaranteed income.

- You have maximized other tax-advantaged accounts like 401(k)s and IRAs.

- You want to secure income for essential expenses.